No Tax Relief on Regulatory Settlements: CBDT Tightens the Belt on Corporate Deductions

4/24/20252 min read

Government Bars Deduction of Expenditures Related to Regulatory Violations

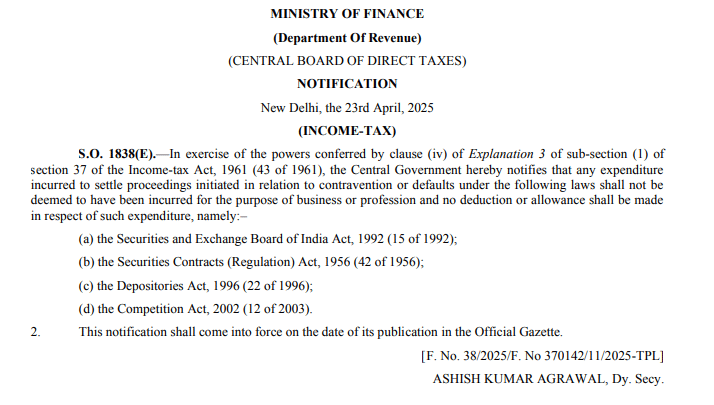

In a significant move aimed at tightening corporate tax compliance, the Central Board of Direct Taxes (CBDT) has issued a notification that bars businesses from claiming tax deductions on expenses incurred to settle proceedings under key financial and competition laws. This decision, announced via Notification S.O. 1838(E) dated 23rd April 2025, brings clarity to the interpretation of Section 37(1) of the Income-tax Act, 1961, and sends a strong message that regulatory breaches will not enjoy any tax shield.

What the Notification Says

The notification was issued under clause (iv) of Explanation 3 to sub-section (1) of Section 37 of the Income-tax Act. It explicitly states that any expenditure incurred to settle proceedings for contraventions or defaults under the following four laws shall not be treated as expenditure incurred for business or professional purposes, and hence, cannot be claimed as a tax deduction:

The Securities and Exchange Board of India Act, 1992

The Securities Contracts (Regulation) Act, 1956

The Depositories Act, 1996

The Competition Act, 2002

In simpler terms, if a company pays fines, penalties, or enters into a financial settlement to resolve violations under any of the above laws, it cannot reduce its taxable income by claiming these costs as a business expense.

The Legal Context

Under Section 37(1) of the Income-tax Act, any expenditure (not being capital or personal in nature) laid out wholly and exclusively for business purposes is generally allowed as a deduction. However, Explanation 1 to this section bars deductions for any expenditure incurred for a purpose that is an offence or is prohibited by law.

To provide further clarity and prevent misuse, Explanation 3 was introduced, which empowers the Central Government to notify laws under which violations or settlements would disqualify related expenses from being treated as deductible. The present notification operationalizes this clause and formally includes the above four legislations in the list.

Implications for Businesses

The notification has far-reaching consequences for corporates, especially those in the financial services, securities, and capital markets space. Here’s what it means:

No tax benefits on settlement costs with SEBI or CCI (Competition Commission of India).

Legal and consultancy fees incurred specifically for regulatory settlements under these laws will not be tax-deductible.

Encourages companies to enhance regulatory compliance as violations now come with both direct financial penalties and indirect tax costs.

This move aligns with the government's broader policy of "no tax shelter for wrongdoers" and aims to prevent companies from treating regulatory non-compliance as a mere cost of doing business.

Strengthening Accountability

By denying tax deductibility for such expenses, the government reinforces the principle that only legitimate business expenditures should be rewarded with tax benefits. It also removes a perceived loophole where companies could partially offset regulatory penalties through tax savings.

Final Thoughts

The CBDT’s latest notification is not just a technical tweak in the tax code—it is a powerful signal that regulatory compliance is non-negotiable. For businesses, the message is clear: Play by the rules, or pay the full price—without expecting a tax break.

As India sharpens its regulatory framework and aims to improve corporate governance standards, this development marks another step in ensuring that the cost of wrongdoing is borne entirely by the wrongdoer, not subsidized by the exchequer.

Consulting

Expert advice on tax and business solutions.

Contact us

Support

info@taxinfinite.com

+91-7817848781

© 2025. Roul Associates All rights reserved.